")

Mohit Oberoi, a seasoned writer with an MBA in finance, has over 18 years of experience. His extensive portfolio includes 8,000 articles published in notable platforms, covering global markets, technology, electric vehicles, metals, personal finance,...

Read Full BioThe Penn Entertainment (NYSE: PENN) stock outlook is uncertain, after activist investor HG Vora successfully had two directors elected at yesterday’s annual shareholder meeting.

The results were in line with expectations as both the company and HG Vora backed both Johnny Hartnett and Carlos Ruisanchez.

For context, HG Vora took a 4.8% stake in Penn, which makes it the third-largest investor behind BlackRock and Vanguard.

The fund has been critical of Penn’s management, including for what it called “misguided transformation into a sports, media and technology conglomerate.”

HG Vora Laments Poor Executive Management

In its presentation, HG Vora said that Penn’s online sports betting pivot has “failed” despite spending $4 billion on the venture over five years.

It particularly listed the Barstool Sports acquisition, where Penn eventually sold back the venture to Dave Portnoy for a mere $1 after having paid over $550 million initially.

The fund also lashed out at Penn’s executive compensation, especially in light of its sagging stock price.

HG Vora was looking to add a third nominee, Penn’s former CFO William Clifford, to the board, but Penn reduced the number of directorial candidates from three to two.

While Penn will officially file the results in the coming days, HG Vora claims Clifford’s candidature also received the support from the majority of shareholders.

Importantly, what appears to be a setback to Penn’s management, HG Vora’s release claims that 60% of shareholders rejected its “Say-on-Pay” proposal.

While two directors won’t exactly give HG Vora veto powers, the fund is expected to pursue changes related to Penn’s online betting business, its partnership with ESPN Bet, and push for deleveraging.

Meanwhile, Penn shares are trading slightly lower in pre-market today as the results of the shareholder meeting were expected.

The muted price action could also be because HG Vora does not have any previous track record as an activist investor, and it is the firm’s first foray into activism.

Markets might wait and see how its nominees help change Penn’s business before reacting to the new directors.

Penn Entertainment’s Underperformance Made It Ripe for Activist Investors

Penn always looked fertile for intervention from an activist investor given its disappointing price action.

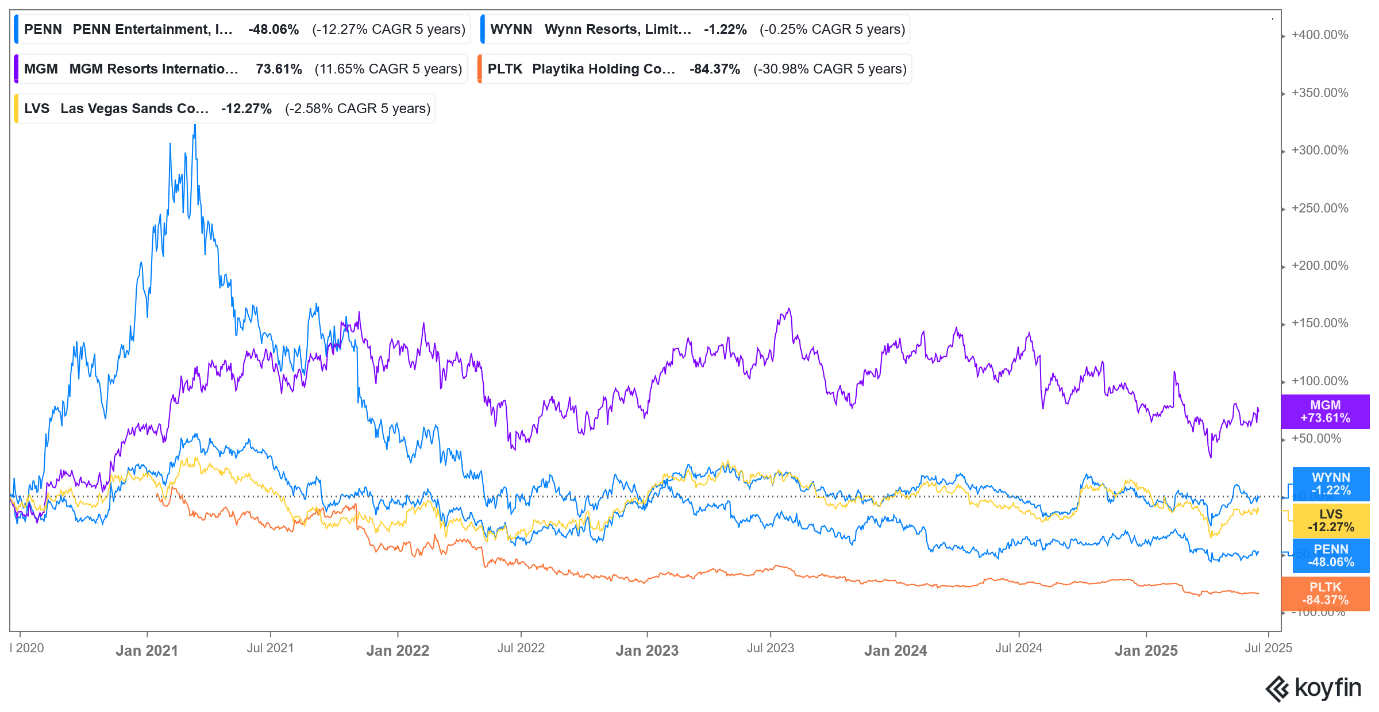

The stock has lost around half of its market capitalization over the last five years and is down a whopping 89% from the record highs it reached in 2021.

For context, Las Vegas Sands and Playtika Holdings have lost 12% and 84 % over the last five years. Wynn Resorts is flat, while MGM Resorts has gained almost 74% for the period.

While competitors’ performance has been mixed, Penn has underperformed compared to the majority of its peers over the last five years. HG Vora attributes this to the board’s failure to hold management to account for astute execution.

Why Has Penn Stock Been Falling?

Penn’s dismal price action since the 2021 peak is not surprising, given that its financial performance has underwhelmed, frequently missing earnings estimates (including in Q1 2025).

The company’s revenues rose 65% in 2021, the year it hit its record highs. However, growth fell to 8.4% in 2022, and in 2023, its revenues declined by 0.6%. Revenue growth did recover to 3.4% last year, and analysts expect topline growth in the ballpark of 5% in 2025 and 2026.

The bottom-line performance has deteriorated badly, and its adjusted net income fell from $428.3 million in 2021 to $401.8 million in 2022 and $60.8 million in 2023. Last year, the company reported an adjusted net loss of nearly $252 million, while its free cash flow was -$123.4 million.

What’s the Forecast for Penn Entertainment Stock?

There has been no major analyst action following the AGM, as the results were in line with estimates.

In its release welcoming the two new directors, Penn said, it is “intently focused on driving profitability in our Interactive segment and growth across the business.” It also talked about the need to deleverage its balance sheet and return capital to shareholders.

The company repurchased $35 million worth of its shares in Q1 and intends to scale up repurchases in the second half of the year, as it views its stock price as “severely dislocated” from its fundamentals.

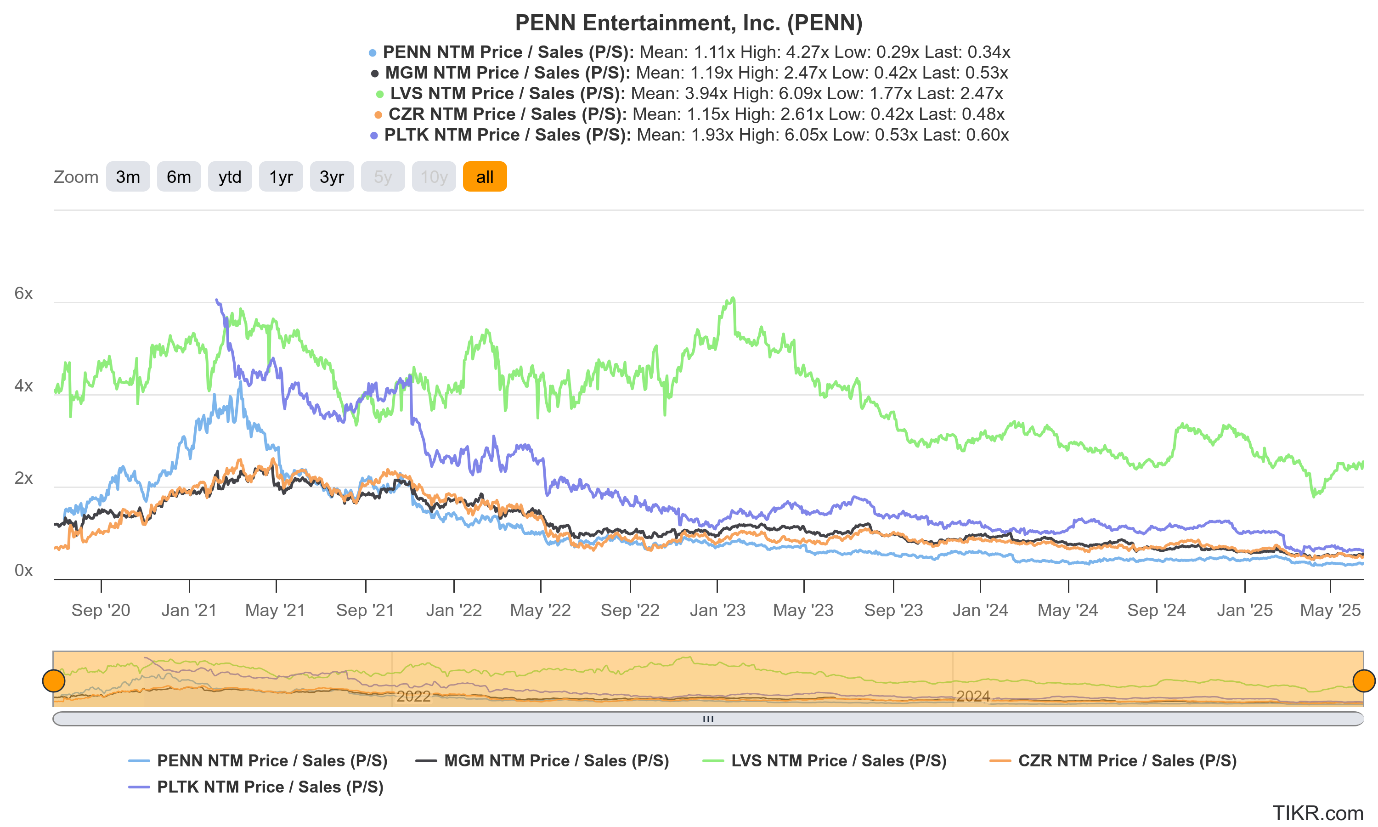

Penn’s valuations have plummeted amid perennial underperformance, and it trades at just 0.34x its projected sales over the next 12 months, which is not only the lowest among its major listed peers but is also a discount to its long-term average multiples.

While HG Vora and the analyst community agree with Penn’s management on its valuations, given the over 41% discount to the median target price of $23.23, the company might need to change its strategy to drive shareholder returns.

That said, the record of activist investors in driving turnarounds is mixed at best. While there are success stories, such as Dan Loeb pushing Yahoo to divest its Alibaba stake, there have been many failures, including Bill Ackman’s ill-fated efforts to transform J.C. Penney.